Are California Fires a Risk to the Muni Market?

The wildfires in California continue to exact a devastating physical and human toll, and that should be the primary focus as this disaster unfolds. However, it's likely that some investors have questions about any potential impact on financial markets, and we will attempt here to explain some possible effects.

We believe that the wildfires may have an impact to some municipal bond issuers in the area, but that the broader impact to other bonds in the state or to the national muni market is likely limited. However, for investors who are concerned about the impact of the wildfires, or weather and climate disasters more generally, there are actions they may want to consider taking.

Where things stand now

According to the California Department of Forestry and Fire Protection (CAL FIRE), as of January 15 there were 153 active fires, which had burned 40,660 acres and destroyed more than 12,300 structures. The largest wildfires—the Palisades Fire, the Eaton Fire and the Hurst Fire—were all located in Los Angeles County and had burned more than 38,000 acres. Containment varied between 19% and 97% for the four largest fires, and some experts predicted they could grow in size due to weather forecasts at the time for continued high winds and a lack of precipitation in the area.

The largest fires were in Los Angeles County

Source: California Department of Forestry & Fire Protection. Data as of 1/15/2025, 10AM PST.

Earthstar Geographics, powered by Esri, Genasys and Perimeter. The information presented here reflects what is known to CAL FIRE and is updated frequently at https://www.fire.ca.gov/. For illustrative purposes only.

Which issuers are most at risk?

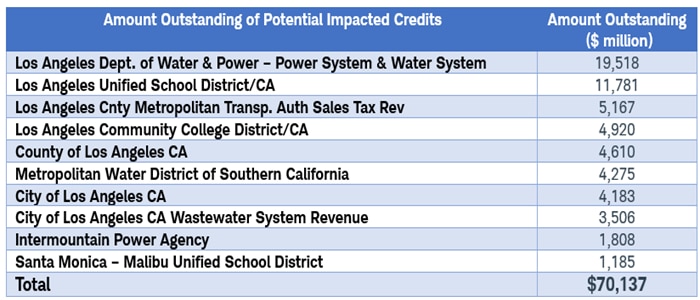

There currently are more than 4,527 individual bonds outstanding (measured by CUSIP number), accounting for $70 billion, in the fire-affected area, according to research provider Bloomberg Intelligence. The risk to each individual issuer is not the same and will depend on the issuer's financial position, how the issuer derives revenues, the bond's legal protections, and other factors. We want to emphasize this point: Even though an issuer may be located in Los Angeles County, there may be minimal risk to its bonds.

Area muni issuers have about $70 billion in outstanding bonds

Source: Bloomberg Intelligence, as of 1/15/2025.

All issuer names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Although there are many bonds outstanding, we're going to focus on three categories of issuer and the potential risk associated with each one.

Los Angeles Department of Water and Power

Risk level: Elevated

The Los Angeles Department of Power and Water (LADWP) is the largest issuer in the area and has two main types of bonds outstanding: water revenue bonds and power revenue bonds. On January 14, Standard and Poor's downgraded1 the power system revenue bonds to A from AA- due to the "utility's potential vulnerability to financial liability claims that could eclipse its liquidity and insurance coverage." The state of California has relatively strict laws about the liability of a utility company regarding wildfires. Our understanding is that if a utility's equipment is found to have been the cause of the wildfire, that utility may be financially responsible for the wildfires even if it was not negligent and the fire is considered an "act of God." While no cause of the wildfires has been determined, if LADWP's equipment is found to have caused the wildfires, it may be at risk. The financial impact will be a function of the cost of the wildfires, the financial resources it has available to it, and any insurance policies it has.

In addition to downgrading LADWP's power revenue bonds, S&P also downgraded its water revenue bonds to AA- from AA+ due to "heightened potential for litigation, liabilities, and future costs surrounding the adequacy of existing water system assets and emergency preparedness during the ongoing wildfires." When the wildfires initially broke out, the Santa Ynez reservoir, which is a part of the Los Angeles water supply system, was closed and offline for repairs. Reports were that many fire hydrants in the Palisades neighborhood were dry or had inadequate water pressure, which exacerbated firefighters' difficult job in fighting the blazes.

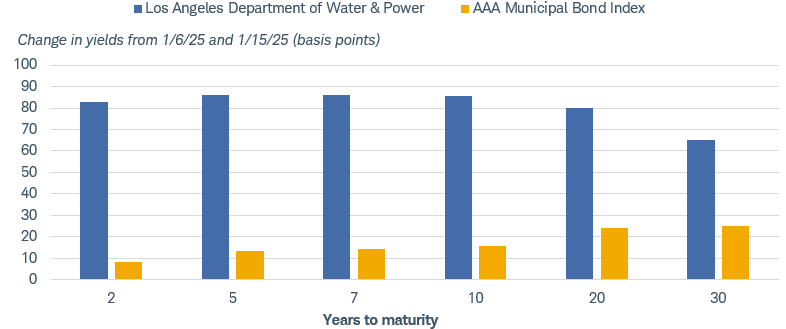

Since the onset of the wildfires, yields for both LADWP power and water revenue bonds have risen, suggesting that the market is assigning a greater risk to these bonds.

Yields for LADWP power and water revenue bonds have risen

Source: Bloomberg. Los Angeles Department of Water & Power BVAL Yield Curve and the Municipal AAA BVAL Yield Curve, as of 1/15/2025.

The Bloomberg Evaluated Pricing Solutions (BVAL) Muni Yield Curve is the baseline curve for BVAL tax-exempt munis and reflects high-quality US municipal bonds. The yield curve is built using non-parametric fit of market data obtained from the Municipal Securities Rulemaking Board (MSRB), new issues calendars, and other proprietary contributed prices. The Los Angeles Department of Water & Power BVAL yield curve is populated with pricing from public power revenue-backed bonds from Los Angeles Department of Water and Power. Past performance is no guarantee of future results. All names and market data shown above are for illustrative purposes only and are not a recommendation, offer to sell, or a solicitation of an offer to buy any security.

Other issuers in LA County or surrounding areas

Risk level: Manageable but still developing

It's likely too early to tell—and we would caution against speculating—but in our view the financial impact to other issuers in the area will be manageable. The impact to other revenue bond issuers in the area will depend on whether there's reduced usage for their services. Some bonds are backed by property taxes in the area, and although the wildfires have burned less than 2% of the acreage in LA County, the largest fire is located in the Palisades area, which contains many high-value homes and business. For example, the median home price in Pacific Palisades is $4.2 million, according to real estate listings website Realtor.com. Following a disaster, a property owner is generally still liable for the taxes on the assessed value of the land even if the structure is fully destroyed. These still may be quite high, because the value of the land in the affected area is high. Once the properties are rebuilt, the homeowner will keep the assessed value, assuming they don't increase the size of the structure built on the land. If they do increase the size of the structure, the additional square footage will be reassessed at current market value. Finally, the assessed value, which property taxes are based on, may be lower than the market value of the property due to how California calculates assessed values. This may limit the financial impact to property tax revenues. However, S&P placed the general obligation bonds for the city of Los Angeles on CreditWatch with negative implications on January 15th due to "heightened risk of credit deterioration for the Los Angeles Department of Water and Power, which could pressure the city's finances, in addition to near-term risk to the city's property tax base and financial position." Being placed on negative CreditWatch means there's a 50% chance the issuer will be downgraded in the next 90 days.

Bonds issued by the state of California

Risk level: Low

Historically, when a weather and climate disasters have occurred, the general obligation bonds for the state have not been affected. If the market anticipated a financial impact you would expect to see yields on the states' general obligation bonds rise, but in past instances that has not been the case. Although these wildfires are expected to be the worst in history, we would not be surprised if the impact to the state's finances is limited, as it has been in the past.

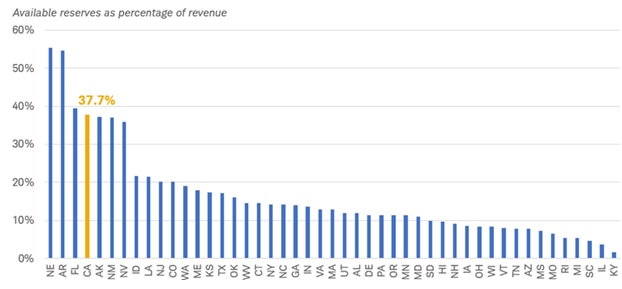

However, a potential risk relates to the timing of receiving income tax revenues and the costs associated with cleanup and restoration. California relies heavily on high-income earners, with the top 1% of income earners in the state accounting for roughly 40% to 50% of the state's total income taxes.2 Additionally, LA County accounts for approximately 30% of the state's revenues.3 As a result of the wildfires, the IRS has granted an extension to homeowners who lost their homes: Instead of the regular deadline in April, they will have until October 15 to file their taxes. As a result, the state will likely experience a delay in when it receives tax revenues. We expect this to be manageable, however, because the state has been building up its liquidity positions over the past few years and can use these funds or other budgetary maneuvers to help offset revenue declines.

California's liquidity position is among the highest in the country

Source: Standard & Poor's Financial Services, as of 12/31/2024.

Chart excludes North Dakota and Wyoming for visual purposes, because their available reserves are so much higher than other states' that including them would skew the scale; North Dakota's reserves are 111.5% of revenue and Wyoming's are 83.9%. Montana is excluded because it has no debt and does not maintain an issuer credit rating from Standard and Poor's.

Are weather and climate disasters a risk to the broader muni market?

We're aware that climate change and weather and climate disasters have become a hot-button issue, but the frequency of disasters has been increasing over the past few years and municipal bond investors shouldn't ignore the fact that natural disasters such as hurricanes, floods, wildfires, and droughts can have a major financial impact on the areas in which they occur.

Historically, most municipal issuers affected by natural disasters have been able to manage through the financial impact caused by the disaster. No state or local government rated by Moody's Investors Service has defaulted on its bonds due to a natural disaster. However, ratings downgrades are a possibility (when a bond is downgraded, its yield tends to rise and its price generally falls).

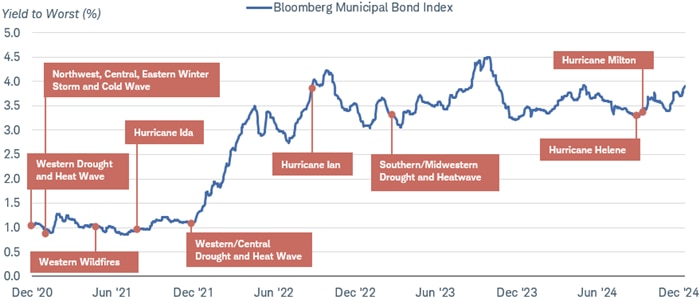

Natural disasters don't appear to pose a risk to the broad muni market either. We haven't seen yields rise across the board following past natural disasters. Higher yields would mean that muni investors, on average, are more concerned about the increased risks. However, historically, yields have been relatively unchanged following a major natural disaster.

The broad muni market has been resilient to past natural disasters

Source: Bloomberg US Municipal Bond Index, NOAA National Centers for Environmental Information, as of 12/31/2024.

Examples of disasters are taken from NOAA National Centers for Environmental Information (NCEI) U.S. Billion-Dollar Weather and Climate Disasters (2025). Past performance is no guarantee of future results. Indexes are unmanaged, do not incur management fees, costs, and expenses and cannot be invested in directly.

Smaller regional issuers are more at risk

Although natural disasters haven't posed a risk to the broad muni market or large issuers like states in the past, we believe they could pose a risk to some smaller regional issuers. When a hurricane, flood, or drought shock occurs, it can result in damaged infrastructure, economic disruption, and outmigration, among other issues. These are all problems that could lead to lower revenues, increased expenses, or a combination of both. Issuers with smaller tax or revenue bases are more at risk compared to issuers, like states, with broad revenue bases.

What should an investor consider doing?

If you own bonds issued by issuers located in LA County, we believe that you should first understand what bonds you own. Not all issuers are going to be affected to the same degree, and the legal protections that some bonds have could help to mitigate the impact to investors. A lot is still unknown at this point, but if you're concerned that things could get worse, we suggest weighing the pros and cons of making changes now versus waiting until some point in the future. However, be aware that the market for some issuers has already adjusted to account for the uncertainty and liquidity may be an issue.

For other investors who don't own bonds that are directly impacted by the wildfires but are concerned about weather and climate disasters in general, we suggest the following steps:

- Diversify by area. When investing in individual bonds, we recommend holding at least 10 different issuers with differing credit risks. This includes issuers in different locations. As a reminder, we recommend that most investors in all states, other than New York and California, diversify nationally.

- Choose areas that are less likely to be impacted by weather and climate disasters. It's no surprise, but location matters. For example, areas in the Midwest are most likely to be affected by extreme heat, whereas coastal areas are most likely to be affected by sea level rise. We don't advocate avoiding issuers in disaster-prone areas completely, but be cognizant of the risks when you are looking at issuers there.

- Focus on higher-rated issuers and do additional due diligence. Historically, issuers with more financial flexibility—a quality that is often associated with higher credit ratings—have been better able to manage through financial disruption. Muni issuers whose finances were already under pressure, which are usually already lower-rated, may be at risk of downgrades—and therefore price declines—because of the added strain. When a bond is downgraded, it reflects the opinion of the credit rating agency that the issuer has less financial flexibility to meet its debt service.

- Explore issuers whose revenues are less impacted by weather and climate disasters. General obligation bonds, for example, tend to be backed by property or sales taxes and historically have been less financially impacted by disasters. Some revenue bonds, on the other hand, are more likely to be affected. A revenue bond is a type of municipal bond issued by an entity that earns revenues from more businesslike operations to pay their bonds back, such as a water and sewer facility, an airport, a college, or a not-for-profit hospital. Broadly speaking, we think that more businesslike enterprises, like a health care facility, airport, or toll road, are at a greater risk than a state government or local general obligation bond from the financial impacts caused by a natural disaster.

- Consider shorter-term bonds. A longer-term risk is that individuals will relocate away from areas that are prone to weather and climate disasters because the financial cost and emotional toll of rebuilding is too great or homeowners' insurance is too expensive. Over time a declining population can result in a smaller tax base. Population trends often take years to develop, so a focus on short-term munis can help reduce this risk. We suggest caution with longer-term munis that are lower-rated and are in areas where shocks are more likely.

Unfortunately, weather and climate disasters like hurricanes, floods and fires are likely to continue. However, muni investors can take steps to lessen the risk on their portfolios. Investing in a mutual fund or exchange-traded fund (ETF) that is well-diversified can help reduce the risk that a small number of issuers will face credit pressures due to a disaster; consequently, it is less likely to have a large impact on the fund's value. However, there may be benefits to investing in individual bonds that outweigh investing in an ETF or mutual fund. For help selecting the right investments for your goals reach out to your Schwab representative.

1 The Moody's investment grade rating scale is Aaa, Aa, A, and Baa, and the sub-investment grade scale is Ba, B, Caa, Ca, and C. Standard and Poor's investment grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C. Ratings from AA to CCC may be modified by the addition of a plus (+) or minus (-) sign to show relative standing within the major rating categories. Fitch's investment-grade rating scale is AAA, AA, A, and BBB and the sub-investment-grade scale is BB, B, CCC, CC, and C.

2 Source: California Governor's Budget Summary, 2022-2023

3 Source: California State Controller's Office, data obtained on 1/15/2025